|

International Pipeline Network in Northeast

Asia

Major achivements and findings

Major

achievements and findings of this research are summarized as

follows:

- We consolidated natural gas supply and demand prospect information on NEA countries (Russia, China, South Korea, Japan and Mongolia) in 2020/2030. Russia and China are countries in NEA with high natural gas production.

Natural gas production in East Siberia and the Far East of Russia will grow rapidly towards 2020/2030. Natural gas production in East Siberia and the Far East will reach 150 BCM in 2020 and 162 BCM in 2030. In 2020, about 50 BCM of it will be exported to other countries by pipeline and 21 BCM of it will be exported to other countries in the form of LNG. In 2030, about 50 BCM of it will be exported to other countries by pipeline and 28 BCM of it will be exported to other countries in the form of LNG. The total amount of export potential will be 71 BCM in 2020 and 78 BCM in 2030. They will be able to cover around 20% of the gas demand of rest four countries.

China will also see rapid growth in natural gas production, reaching 150-180 BCM in 2020. According to the previous joint research (2007 version), the amount of production in 2020 is about 20-25% more compared with our previous research. It is worthy of mentioning that the resources of coal-bed methane are also abundant in China. The major gas production area in China will be the northwest, southwest, and southeast coastal areas including Tarim Basin and Ordos Basin. Natural gas produced in China, however, is expected to be consumed within China as natural gas demand in China will increase rapidly.

- Major energy consuming countries in NEA are China, Japan, and South Korea. Natural gas demand in China will increase dramatically reaching 230 BCM in 2020. This is almost three times higher as compared to the current level. Russia will also see a significant growth in domestic natural gas demand resulting in 27 BCM in 2020 and 32 BCM in 2030 which are around four times as compared with the current consumption level. Natural gas demand in South Korea will grow steadily towards 2030 and its amount is expected to reach 49 BCM in 2020 and 57 BCM in 2030, which are around one and a half times as compared with the current level. The prospects for Japan show the most modest growth among the NEA countries. Natural gas demand in 2020 is expected to be 83-114 BCM in 2020 and 66-117 BCM in 2030. In all the NEA countries combined, the total natural gas demand in 2020 is expected to reach 389 420 BCM.

- We estimated the interregional natural gas flow in 2020 including both PNG and LNG. As compared to the current situation, the increase in natural gas demand in China is remarkable. The majority of the export from Russia to the Asia Pacific region is PNG except for Sakhalin and Vladivostok LNG. PNG is internally transported in China for domestic use. LNG continues to play the main role of natural gas trade in Japan and South Korea. China expects to import more LNG from Australia and the Middle East.

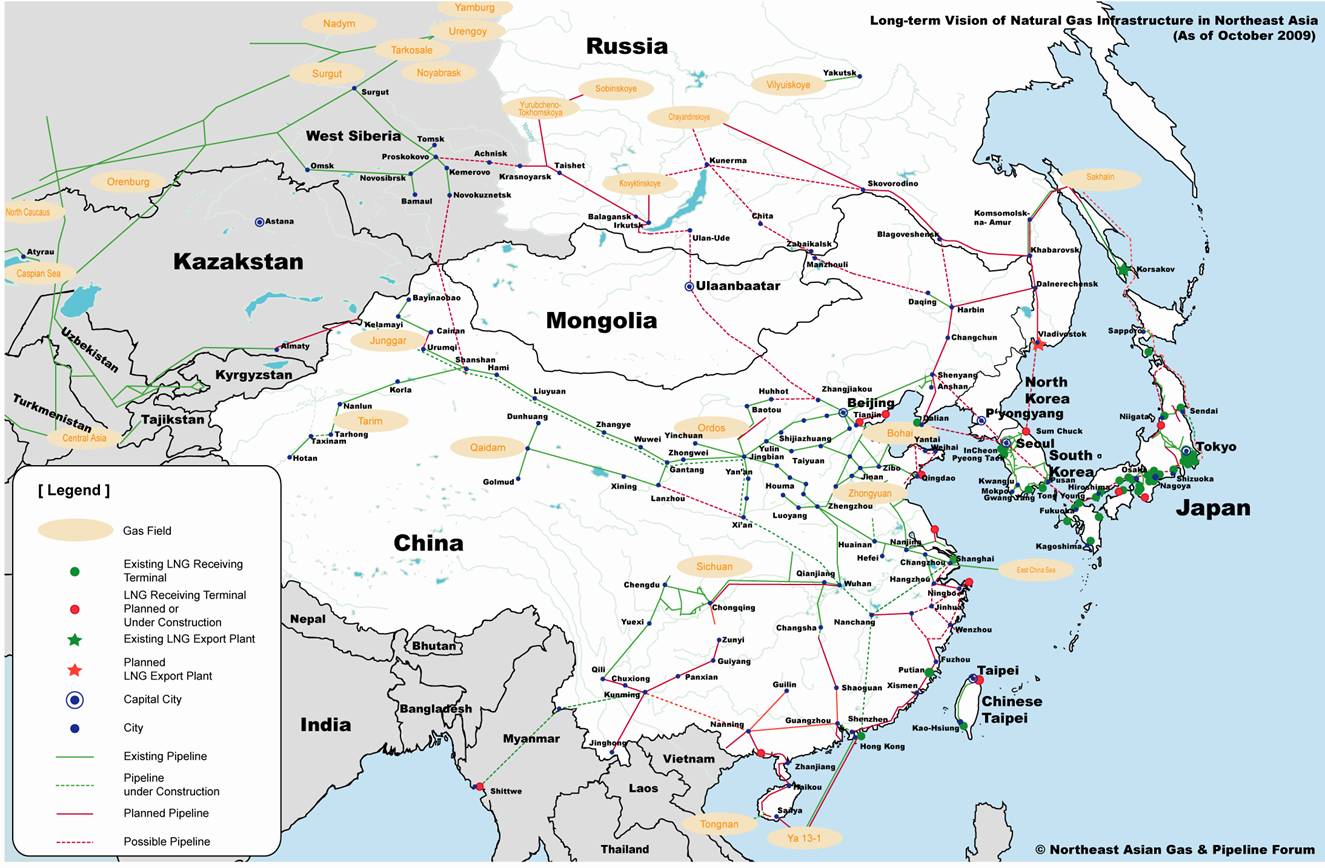

- Based on the natural gas supply and demand prospects, we developed a long-term vision of natural gas infrastructure including LNG as well as PNG. Distinctive points of each country are as follows;

Russia

The project to transport gas 800 km by pipeline from Sakhalin 2 to the southernmost part of Sakhalin Island and liquefy it was completed, and the first LNG ship arrived in Japan early April 2009.

The construction of the following four gas production centers (GPC) and the development of a unified gas supply system (UGS) for delivery of gas from these centers will begin.

- Krasnoyarsk (Oil and Gas Condensate Deposit)

- Irkutsk (Gas Condensate Deposit)

- Yakutsk (Oil and Gas Condensate Deposit)

- Sakhalin (Sakhalin 1 and 2, and promising Sakhalin 3 to 6)

Russia is planning to complete the infrastructure for exporting a total of 9 BCM/a to China and Korea by 2015 and a total of 50 BCM/a to the both countries (38 BCM/a to China and 12 BCM/a to Korea) by 2020. These supplies will continue in 2030. A gas pipeline has already been installed from the northern part of Sakhalin Island to Khabarovsk, and will be used for a while. However, a new pipeline from Khabarovsk to Vladivostok is necessary. Its construction began in July 2009.

Other GPCs in Krasnoyarsk, Irkutsk and Yakutsk will be developed in the future. Plans to build infrastructures to extract and transport valuable components such as helium associated with gas production are included in the development projects.

The main gas source for Vostok 50 is Sakhalin Gas Producing Center. Gas for China is planning to be transported in the form of PNG from the middle point between Khabarovsk and Vladivostok to Northeastern China. For Korea, gas can be transported in the form of PNG to Vladivostok. Whether to deliver it to Korea in the form of LNG or by off-shore pipeline will be determined based on a feasibility study to be performed. For Japan, it is expected that gas can be transported from Vladivostok in the form of LNG.

China

In order to promote the use of natural gas, China has actively been building gas pipeline networks. The 3,900 km West to East Gas Pipeline between Sichuan and Shanghai which was completed in 2004 is symbolic of Chinas policy on pipelines. As of 2007, the total length of Chinas natural gas pipeline was 32,000 km.

The construction of the Second West to East Gas Pipeline started in February 2008 and will be completed at the end of 2009. In 2010, the total length of Chinas natural gas pipelines will be over 40,000 km.

The construction and operation of the following trunk pipelines is included in the pipeline project:

- Sichuan-To-East Gas Pipeline

- Sichuan-To-South Gas Pipeline

- West to East Gas Pipeline (The 2nd Pipeline)

- Northeast Gas Pipeline Networks

- Pipeline for imported gas and off-shore pipelines and to improve regional pipeline networks

As a result, in 2020, the total length of Chinas natural gas pipelines will be over 60,000 km. In addition, with the construction of a pipeline to transport coal-bed methane and its connection to the off-shore pipeline, and the construction of distribution pipelines from LNG receiving terminals, by 2030, the total length of Chinas natural gas pipelines will be 80,000 km.

Ten LNG receiving terminals in coastal regions are being constructed. Three terminals - Shenzhen, Fujian and Shanghai - were completed, and the first phase of construction of Dalian Terminal was completed. Other terminals will be completed by 2020. Natural gas from these terminals will be connected to the trunk gas pipelines in each region.

Korea

The gas market in Korea is becoming matured. The construction of LNG receiving (regasification) terminals and pipeline networks to connect them to the markets is in the final stage.

In Korea, four LNG receiving terminals are in operation. Two of them are located on the west coast and the other two are located on the south coast. Three of the four are owned and operated by KOGAS. They are PyeongTaek Terminal and InCheon Terminal on the west coast and Tongyoung Terminal on the east coast. Another terminal is GwangYang Terminal on the south coast owned and operated by POSCO. PyeongTaek Terminal is the first terminal constructed in 1986, and InCheon terminal is the largest in terms of send-out and storing capacities and number of berth in Korea.

In addition to these, there is another terminal, which is under construction. It is SamChuck Terminal being constructed by KOGAS on the east coast facing Vladivostok in Russia. This terminal aims to supply natural gas to the northeastern part of Korea, which is isolated by a high mountain range, and will be completed by 2014.

In Korea, main gas pipelines were installed first between densely populated cities surrounding Seoul, and then extended to smaller cities. As of the end of 2008, the total length of the trunk pipelines was 2,705 km.

The pipeline network in Korea is one of the best pipeline systems in the world. It is a loop type and can easily deal with various kinds of pipeline accidents such as cut-off. Between 2014 and 2015 when SamChuck Terminal will be completed and a pipeline will be installed in the northeastern part, almost all main cities in Korea will be connected by gas pipeline systems.

Japan

In Japan, as in Korea, most of the imported natural gas is regasified at LNG receiving terminals and delivered to the markets. Japan purchases 74.4 million tons of LNG per year in 2009 and is the worlds largest LNG consuming nation. The most distinctive feature of the LNG infrastructure in Japan is that a large number of LNG receiving terminals which are located in coastal regions. There are 28 operating LNG receiving terminals in 2009, an increase of 5 over 2007 (23 terminals).

Currently, three LNG receiving terminals are being built. They are Jyoetsu LNG Terminal on the Sea of Japan coast, Wakayama LNG Terminal on the Pacific coast, and Sakaide LNG Terminal on the Seto Inland Sea coast.

Natural gas regasified at these terminals is supplied mainly to the heavy industry areas and large cities in coastal regions. The pipeline is not a loop type, although in small quantities. Domestic natural gas is produced in the plain along the northern coast of the Sea of Japan. Gas is transported, mainly for consumer use, by pipeline to large cities such as Tokyo and Sendai.

Contents

| Chapter1 |

Introduction |

| |

1.1 Background and Objectives |

| |

1.2 Basic Concepts |

|

| Chapter2 |

Current Situation and Prospects of Natural Gas in

Northeast Asia |

| |

2.1 Russia |

| |

2.2 China |

| |

2.3 South Korea |

| |

2.4 Japan |

| |

2.5 Mongolia |

| Chapter3 |

Long-Term Vision of Natural Gas Infrastructure in Northeast Asia

|

| |

3.1 Natural Gas Supply and Demand Balance in

Northeast Asia |

| |

3.2 Long-term Vision of Natural Gas Infrastructure

in Northeast Asia |

| The way

forward | | |